Problem

Savings and pension planning alone are not effective enough to secure the financial health of the population. Notwithstanding pensions, Estonians also wish to save money for other major expenses such as purchasing property, renovations, education, hobbies and travel.

Although investment accounts are becoming increasingly popular, today, people with a higher level of financial literacy primarily make use of them. Meanwhile, tax exemptions do not apply to early withdrawals from Pillar II or III of the Estonian pension system.

Therefore, improving the financial health of the nation requires, in addition to pensions and savings options, also the possibility to conveniently invest in the medium-long term.

Solution

Grünfin, a company participating in Accelerate Estonia’s program, has proposed specific solutions to improve Estonia’s investment environment and increase motivation for long-term investment, involving employers in the process. Employers are excellent partners to make improvements in individuals’ financial literacy and behaviour with the greatest impact and scale possible. In order to engage employers, financial motivation must first be built.

One proposal is to extend the tax exemption for stock options to other investment products that are more broad-based and diversified. Since the risk level of the products would be similar to pension funds, it would also be suitable for a wider group of society.

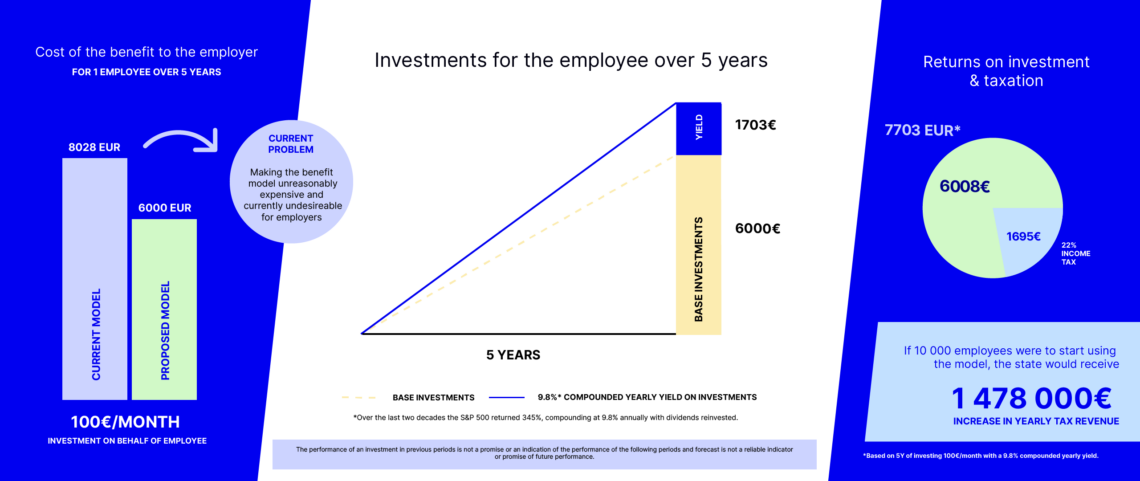

When looking at long-term investments, 51% of Estonians wish for their employers to contribute to their pension savings in place of salary increases. Likewise, this proposal creates a model whereby the employer makes investments for the employee and alongside the employee.

The solution would require the exemption of long-term (for example, more than 3 years) savings programs from fringe benefits tax and taxing them similarly to option programs, only with income tax. The tax exemption applies if the employer makes an investment on behalf of the employee, in addition to their salary. Since the employer’s investment is an additional benefit that would otherwise not exist, it also establishes a new tax revenue base for the state.

This approach creates a new opportunity by enabling convenient and automatic investments, particularly benefiting those with lower financial literacy, limited knowledge, and a lack of confidence to start investing independently.

End goal

Grünfin and Accelerate Estonia believe that the proposed legislative changes would significantly increase the number of people actively engaged in long-term investing. This, in turn, would enhance the overall financial well-being of the population, improve financial knowledge and investment skills, and potentially reduce social inequality and economic pressures.

Following the implementation of this change in law Grünfin will develop a pilot product, which, after successful testing and validation at the national level in Estonia, will make it easier to adapt to the wider sector and possibly also export the solution to other countries.

Furthermore, the proposed regulatory change would create a new market segment in the investment landscape. As a result of the tax exemption, employers have a greater motivation to invest on behalf of their employees and hence do not only inject new capital to the market but also to the state budget in the form of income tax.

During the cooperation, Accelerate Estonia involves the necessary parties and conducts an impact analysis of the given solution on people’s financial behaviour and the economy.